Receive market-implied distributions, not just point forecasts.

MRP converts current market prices into forward-looking probability distributions and derived signals, allowing clients to augment their portfolio analytics, identify asymmetric risk, and monitor changing market regimes.

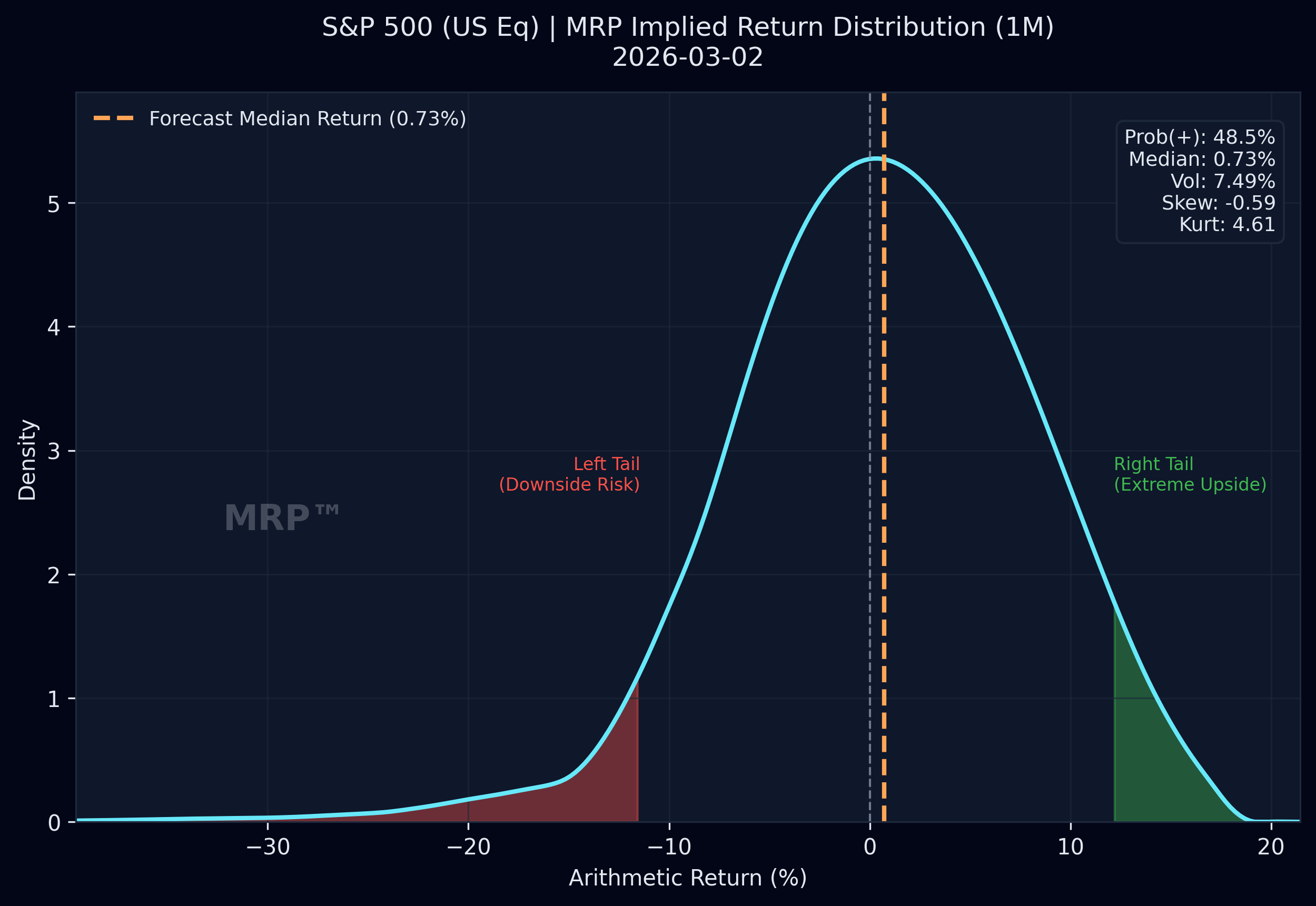

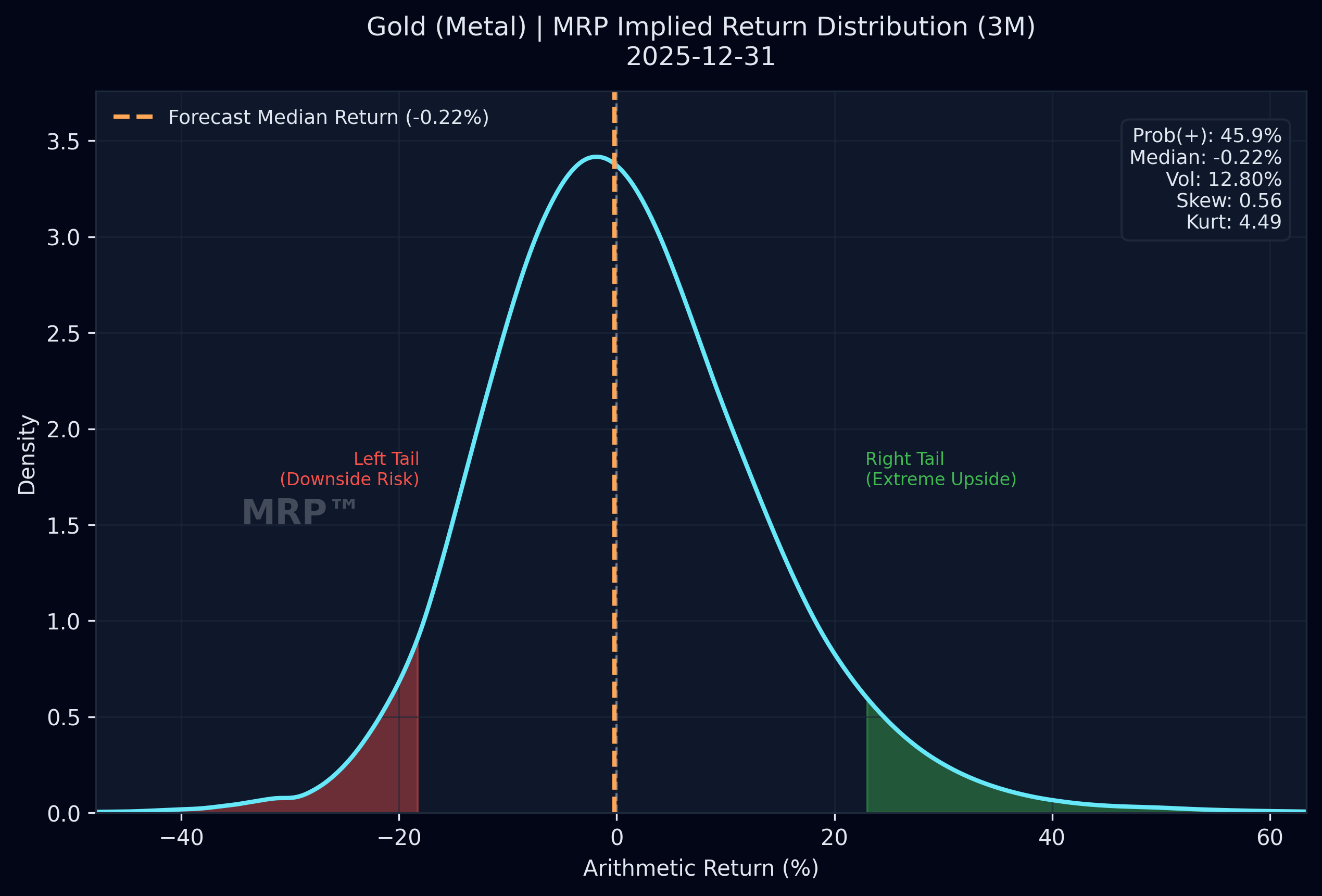

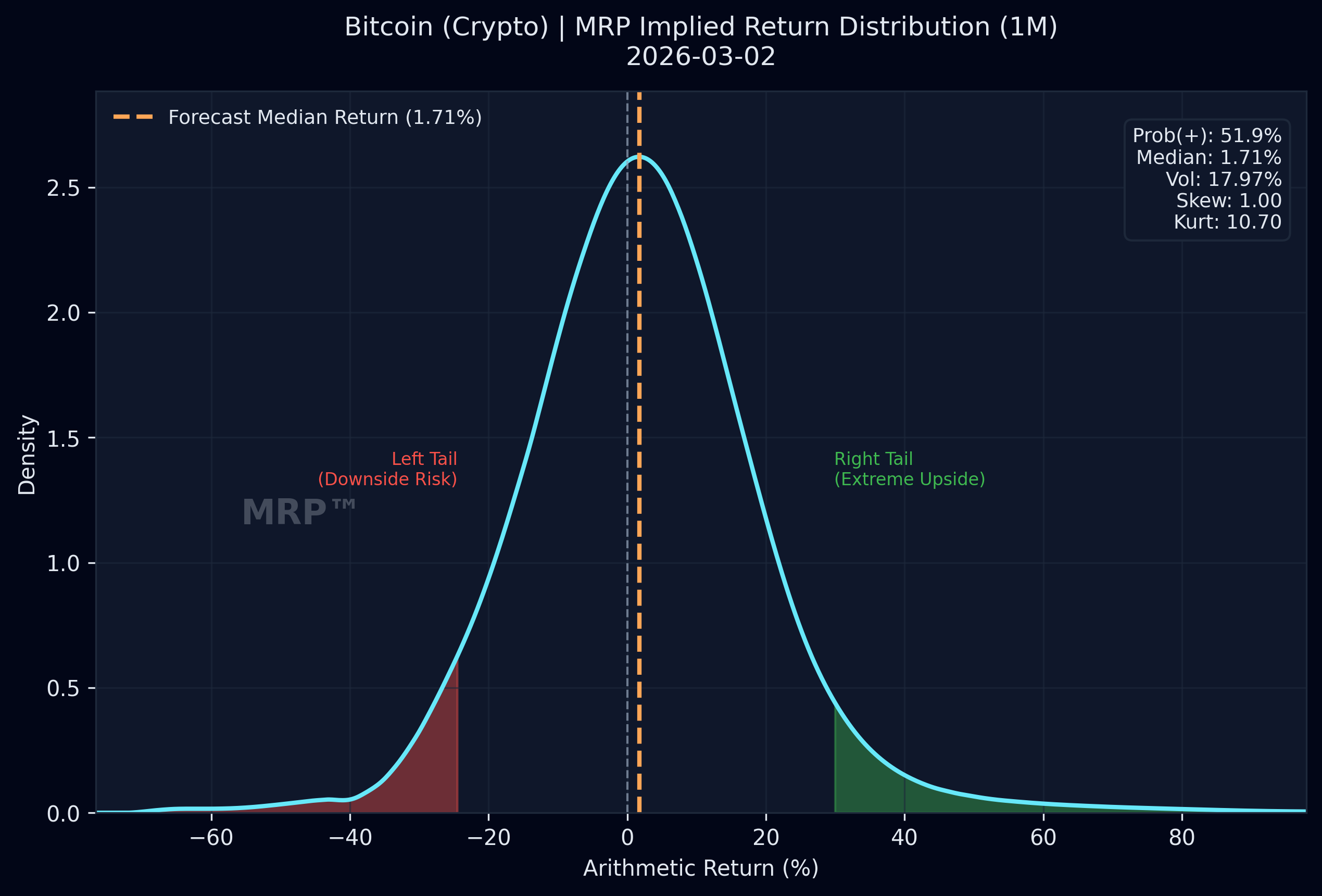

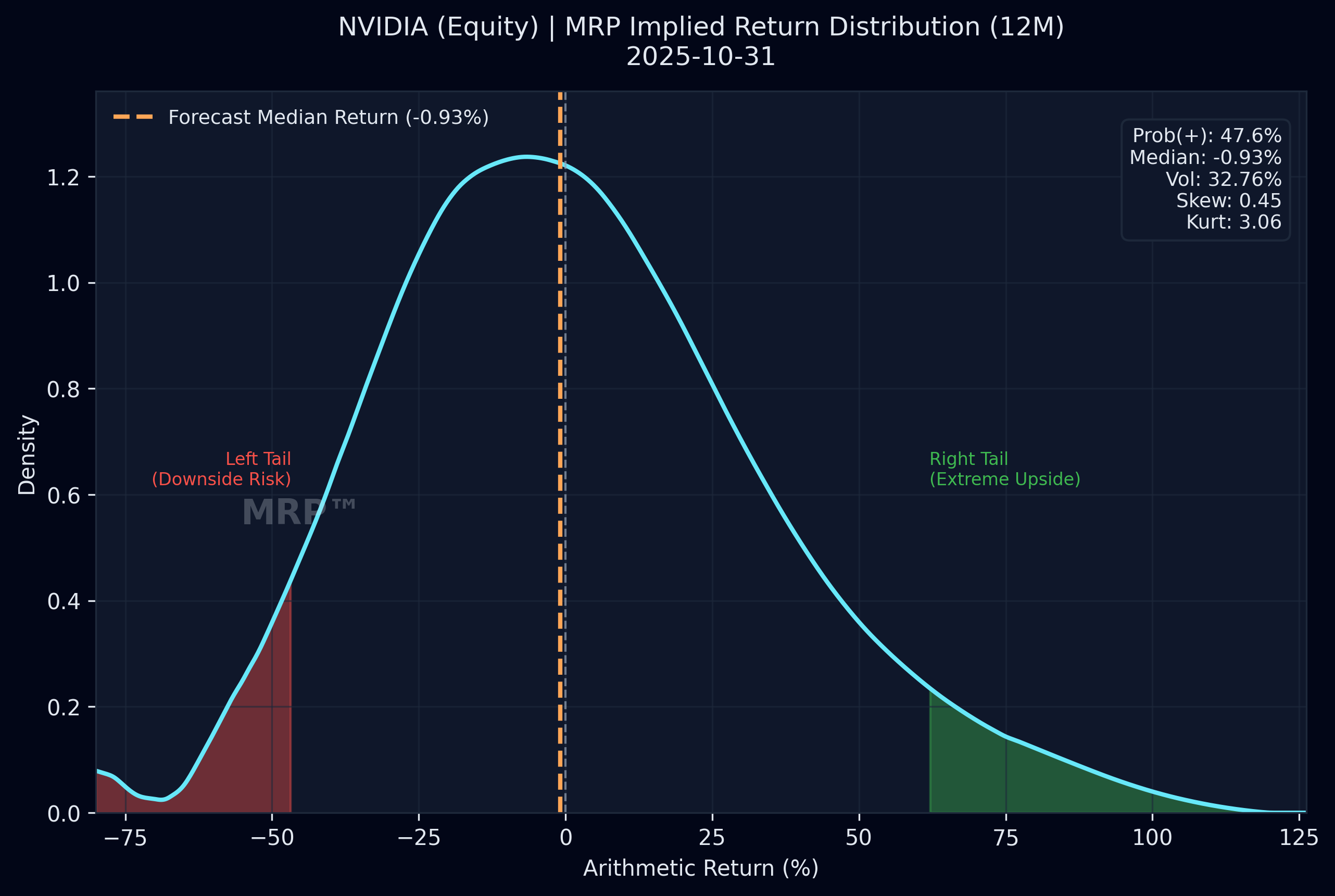

S&P 500 · 1M Gold · 3M Bitcoin · 1M NVIDIA · 12M 20+Y UST · 6M ▾

Current market prices already contain forward-looking information. Most investors do not extract it in a usable form.

Traditional capital market assumptions are often backward-looking, variance-based, and slow to reflect changing market conditions or asymmetric risk.

MRP distributes the full market-implied probability distribution and the time series of its parameters, giving clients a richer input layer for their own analytics.

To improve internal asset-allocation frameworks, enhance scenario analysis, monitor regime shifts, identify selected high-confidence drawdown signals, and analyze periods when returns are persistently favorable.

Built to serve both as a data product and as a probability framework for client analytics.

Forward-looking probability distributions derived from current market prices, delivered as structured output your team can use directly.

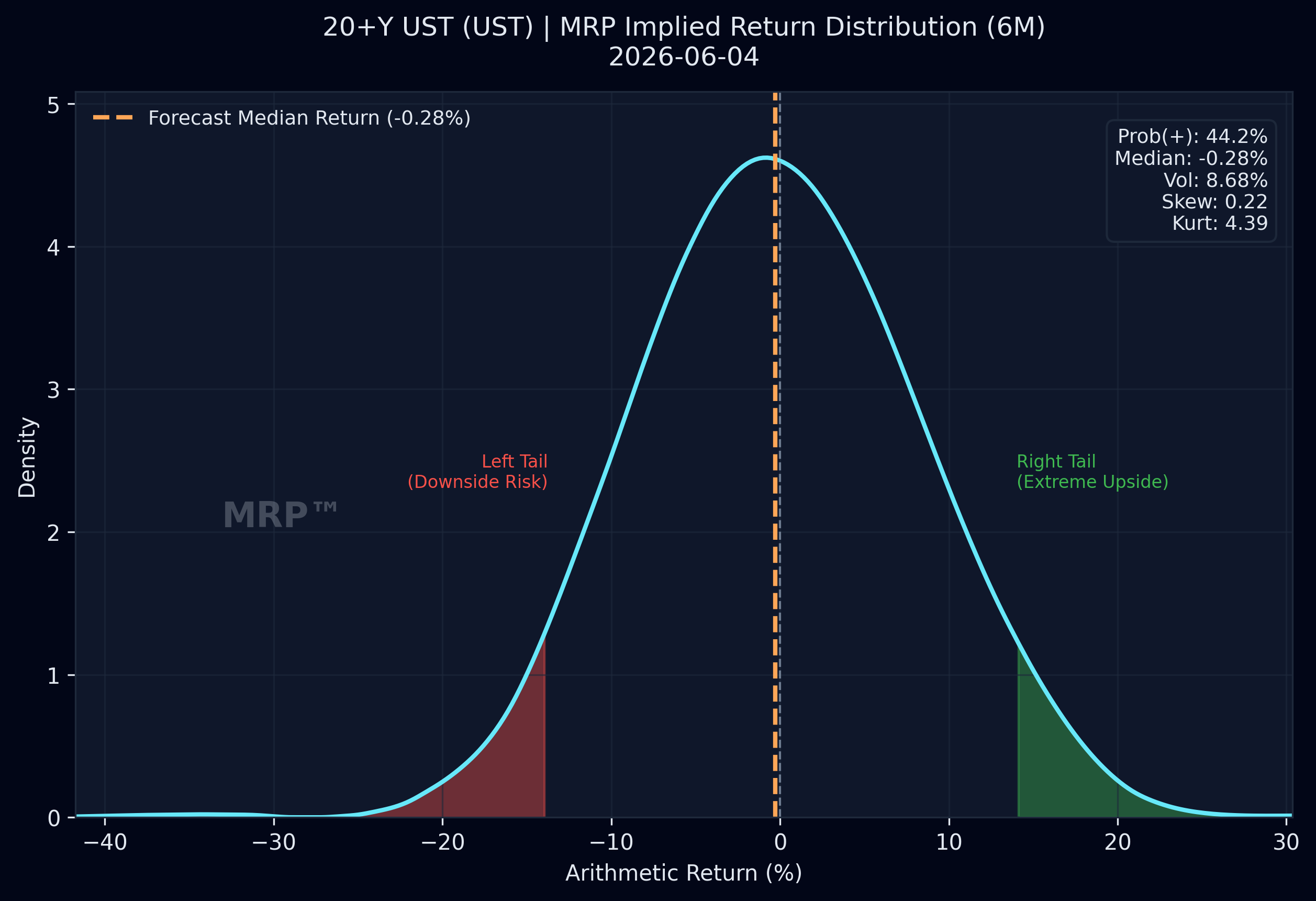

- Distribution curves by asset

- Expected return, volatility, skew, kurtosis

- CSV / Excel / API-ready outputs

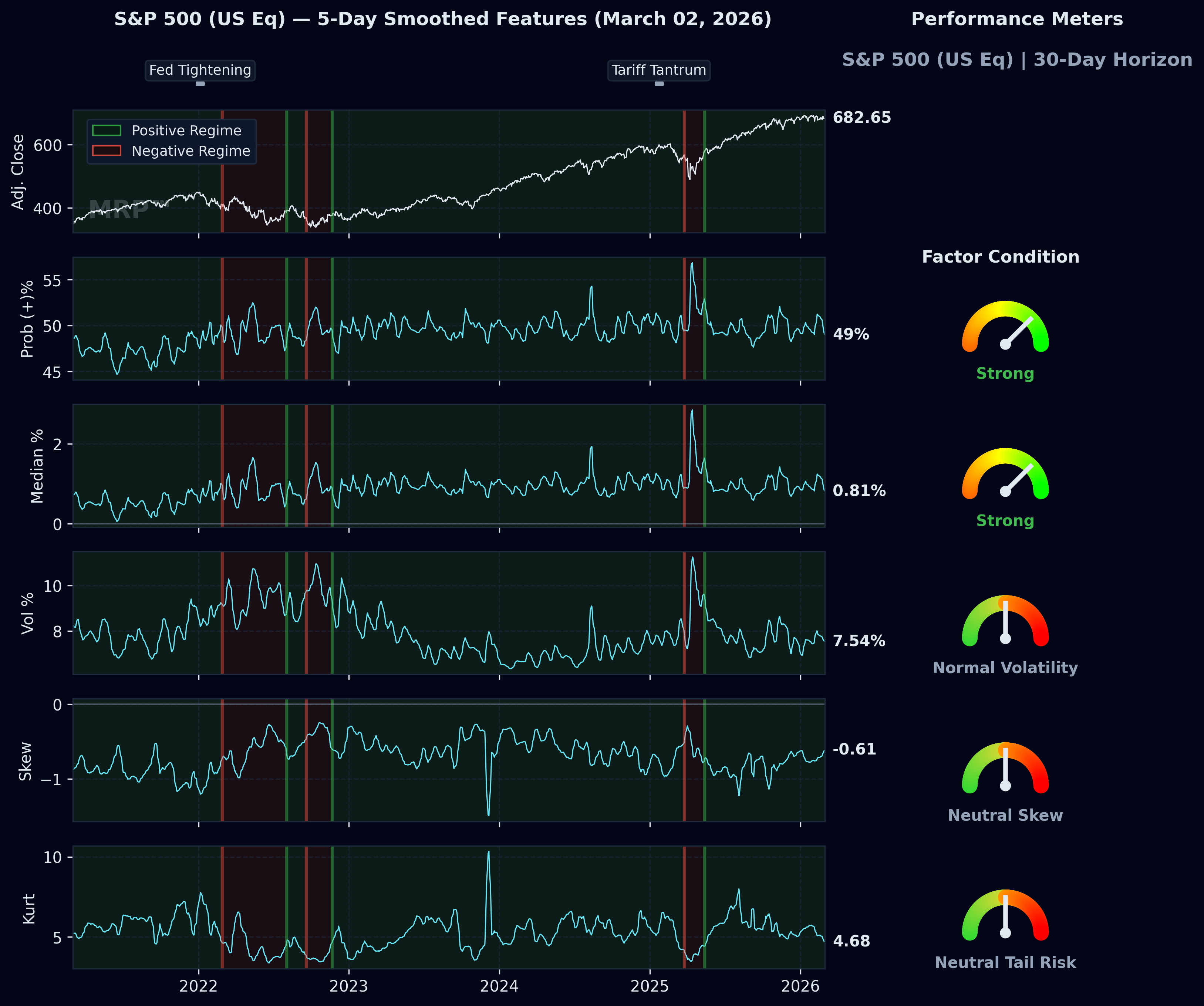

Historical evolution of distribution characteristics, allowing investment teams to evaluate changing market expectations and asymmetry through time.

- Skew and tail-risk history

- Regime pattern recognition

- Enhanced monitoring and research

High-conviction signals can be built from the time series of distribution parameters flagging favorable return environments and selected drawdown risks.

- High-confidence downside warnings

- Positive-return regime identification

- Designed to complement existing process

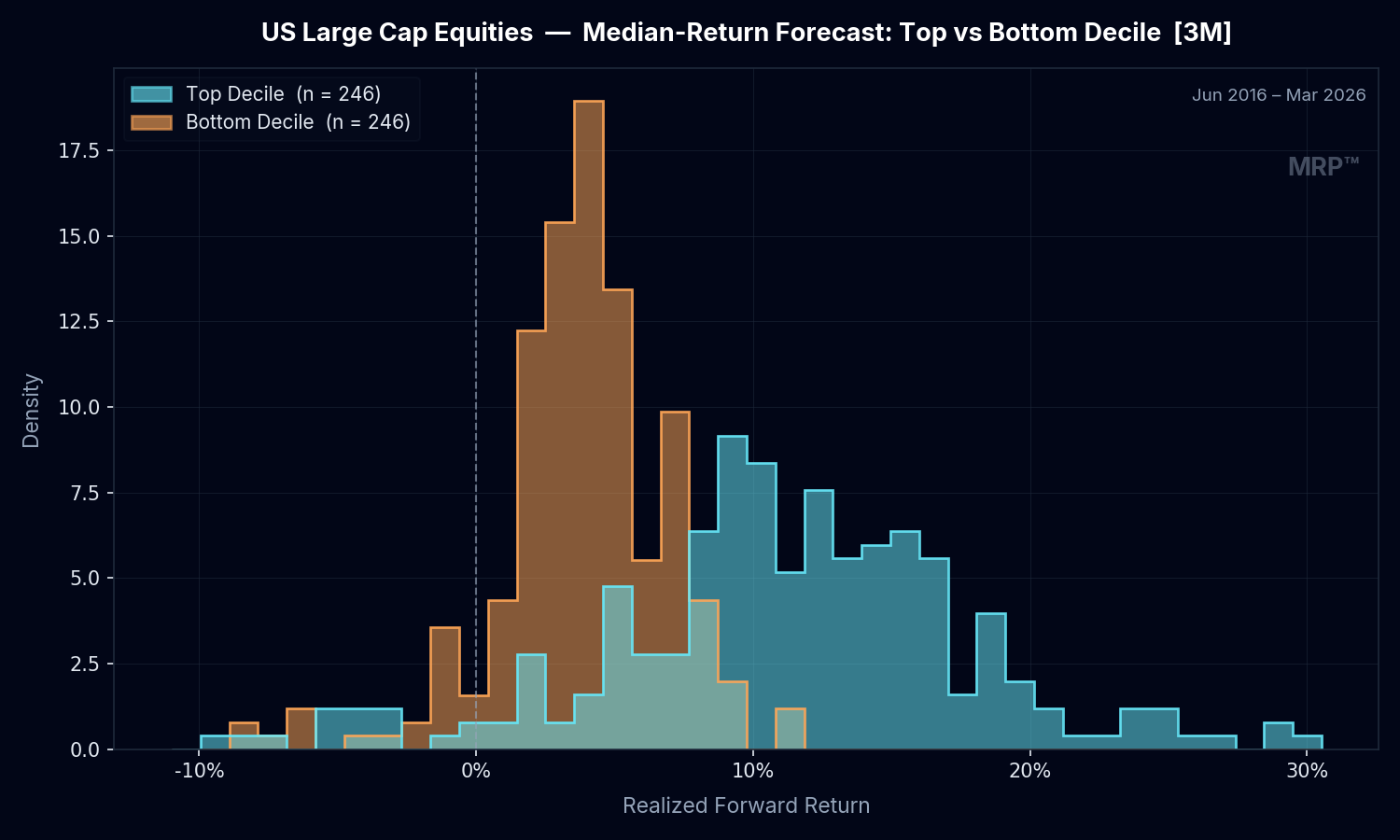

Forward-looking probability examples.

Market-Implied Distribution

Time Series of Distribution Parameters

Realized forward return vs predicted median return

An example of a simple analysis

MRP provides distributions. Strategies presented here are only examples.

Clients retain control of their own process and strategies. MRP enhances decision-making by providing a forward-looking, market-derived input layer and selected derived signals that can be incorporated into existing frameworks.

Signals should be considered high-confidence rather than exhaustive. For example, when an MRP drawdown warning appears, it has generally been associated with subsequent potential drawdown environments, but will not identify every drawdown.

Replace backward-looking assumptions with market-implied distributions that capture asymmetry and tail risk before capital is allocated.

Monitor changes in skew and tail behavior as early indicators that risk is becoming less well compensated.

Incorporate the distributions into your own portfolio construction, scenario analysis, and internal research framework.

Support investment decisions with observable market information rather than relying solely on historical assumptions or qualitative narrative.