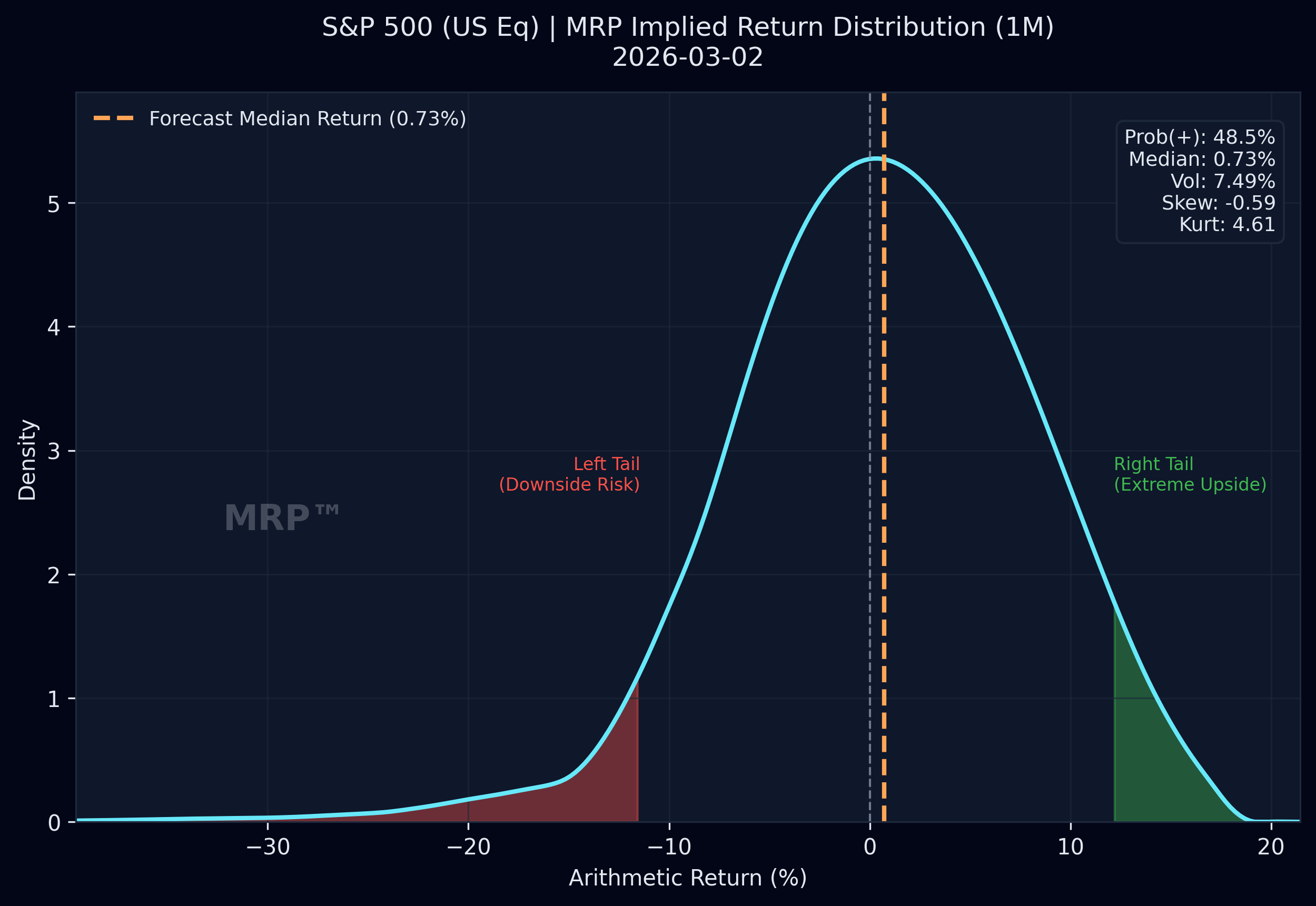

S&P 500 · 1-Month Horizon

Market-Implied Distribution

As of March 2, 2026

Expected Return

+0.73%

Positive market-implied median outcome

Probability of Gain

48.5%

Fewer than half of outcomes are positive

Skew

Negative

Downside asymmetry remains elevated

Tail Risk

Moderate

Tail losses are broadly in line with normal models

The current distribution shows a positive expected return for the S&P 500 over the next month, with 48.5% of the probability mass in positive territory. The negative skew and moderate tail risk indicate that the downside scenarios are materially larger in magnitude than the upside — a pattern worth weighing when considering position sizing and hedging.

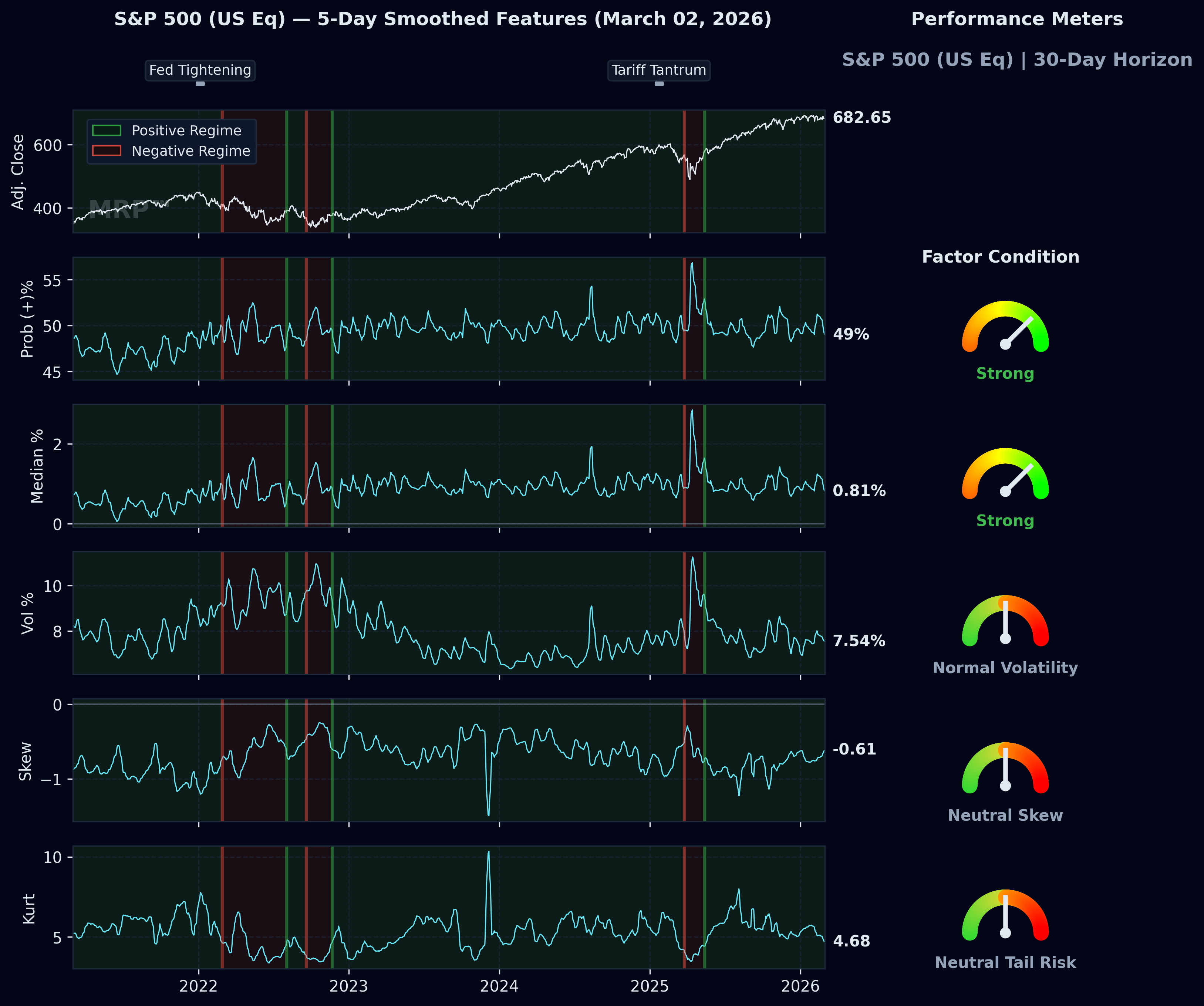

Time Series

Distribution Parameter Monitor

The charts below track how the key parameters of the market-implied distribution have evolved over time — including expected return, probability of gain, skew, and tail behavior. Shifts in these parameters often provide early signals of regime change that variance-only frameworks do not capture.

Parameter time series showing the evolution of market-implied distribution characteristics. Persistent deterioration in skew or a declining probability of gain can serve as early-warning indicators of a shifting risk environment.

Downloads

Available Reports

Full example reports are available below as PDFs. Each report opens in a new browser tab.